.webp?width=832&height=592&name=customer-support%20(1).webp)

Car Finance

Car Finance

Cars & Gadgets

Cars & Gadgets

Car Maintenance

Car Maintenance

Tips & Advice

Tips & Advice

News

News

Road Trips

Road Trips

Pop Culture

Pop Culture

.webp?width=400&height=285&name=online-shoppers-with-dog%20(1).webp)

.jpg?width=500&height=356&name=Vintage%20car%20going%20to%20an%20old%20town-1%20(1).jpg)

Refinancing? We can help.

See if you can switch and save with Carmoola and thank us later.

Switch and SaveTakes 60 seconds, no impact on your credit profile

to see if you're approved 👍

Representative 13.9% APR

How does refinancing work?

STEP 1

Tell us about your finance

Answer a few questions about your car mileage and settlement quote from your current lender

STEP 2

Get a new rate and budget 👍

After a few questions in our app you’ll find out if you’re eligible and your new rate and repayments

STEP 3

Refinance your deal 💸

Simply pay your settlement quote with your Carmoola card or by bank transfer, all from your smartphone

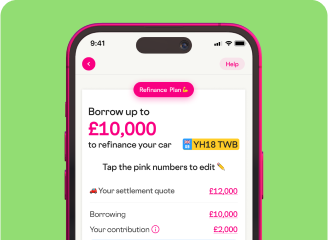

Car refinance calculator 🧮

Thinking about refinancing? See if you can drive away with a better deal.

Your existing finance 🕸

Add details about your current car finance agreement

Customise your

new finance deal ✨

Tweak your contract length and credit profile to see what your new monthly repayments might look like

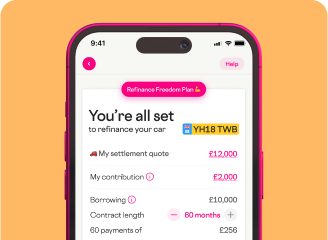

Your new monthly payments

You could reduce your

monthly payments by £443 🙌

Download the Carmoola app to get your

personalised refinance quote, and see how much

you could save!

New deal breakdown ✨

| Borrowing | £10,000 |

| Interest rate | 13.9% APR |

| 48 payments of | £0 |

| Total cost of credit | £0 |

| Option to purchase fee

|

£1 |

| Total payable | £1 |

For illustration purposes only. The rate and budget you may be offered will be based on your individual circumstances. This is not an offer or a quote for finance.

Representative Example

Borrowing £10,000 over 54 months with a representative APR of 13.9%, an annual interest rate of 13.9% (Fixed) and a deposit of £0.00, the amount payable would be £246 per month, with a total cost of credit of £3,284 and a total amount payable of £13,285, including a one-off Option to Purchase fee of £1.

We offer hire purchase and personal contract purchase loans between £2,000 - £55,000 at a personalised APR between 6.9% and 29.9%.

Option to purchase fee

If you'd like to keep the car at the end of the agreement, you'll need to pay a small fee of £1, called the 'option to purchase' fee. The payment of this fee legally transfers ownership from Carmoola, to you, and is automatically added to your final payment.

Why switch to Carmoola?

Anyone can switch their existing car loan by getting an early settlement quote. With Carmoola, you can switch in 8 minutes, all from your smartphone.

Switch and save

Refinancing can unlock savings by restructuring your loan with a lower interest rate or better terms.

5 ⭐️ support

Our friendly, UK-based team is here from 8am - 9pm EVERY day, via WhatsApp, email, SMS or phone.

Payment flexibility

Missed a payment? You can catch up easily in our app and even make overpayments with no fees.

Don’t just take our word for it

“Such a simple way to get car finance and at a good rate too. Easy to use app with step by step process. Love the finance calculator, which allows you to adjust the amounts and see the payments instantly. Would definitely recommend!”

Simon.

“Easy to use and to get a budget with their online calculator! The best part is the flexibility, you can choose how much within your allocated budget and for how long to repay. Will defo use again in the future. *****”

Dean

“Absolutely amazing service, super quick to respond and it couldn’t have been easier, I would 100% recommend Carmoola to anyone!”

Joanne

“Not just a normal car Finance company!! Very fast and efficient and they make you feel like a valued family member, lots of unexpected after sales benefits that have been very much welcomed and appreciated too!!”

Burrow

“Incredible experience! Omg! The way forward in car finance. I’d use these guys again and thoroughly recommend them. 🚘”

Richard

Takes 60 seconds, no impact on your credit profile to see if you're approved 👍

Rates from as low as 6.9% APR, Representative 13.9% APR